Nov 24, 2021

Compliance in the complex French regulatory landscape

The Fourthline Team

France is the 7th largest economy in the world and the EU’s second largest economy, with a GDP that is expected to reach $3.5tn by 2026.

Business opportunities are huge. The 2020 Covid-19 lockdown has accelerated the growth of domestic and cross-border e-commerce. According to the French e-Commerce Federation (FEVAD), internet sales grew 8.5%, generating €112.2 billion. The rise of e-commerce, online payments, and e-banking increase the urgency of robust Customer Identification Programs (CIP).

Card-not-Present (CNP) payment methods are more vulnerable to fraud and ID falsification. Banks, PSPs, and merchant acquirers have to comply with card scheme regulations and with changing KYC/AML rules in different jurisdictions. This becomes particularly challenging for international financial institutions that sell, trade or exchange currencies cross-border. Financial institutions that want to expand their footprint into the French market will have to gain a deeper understanding of the French regulatory compliance landscape.

Compliance with French and EU regulations

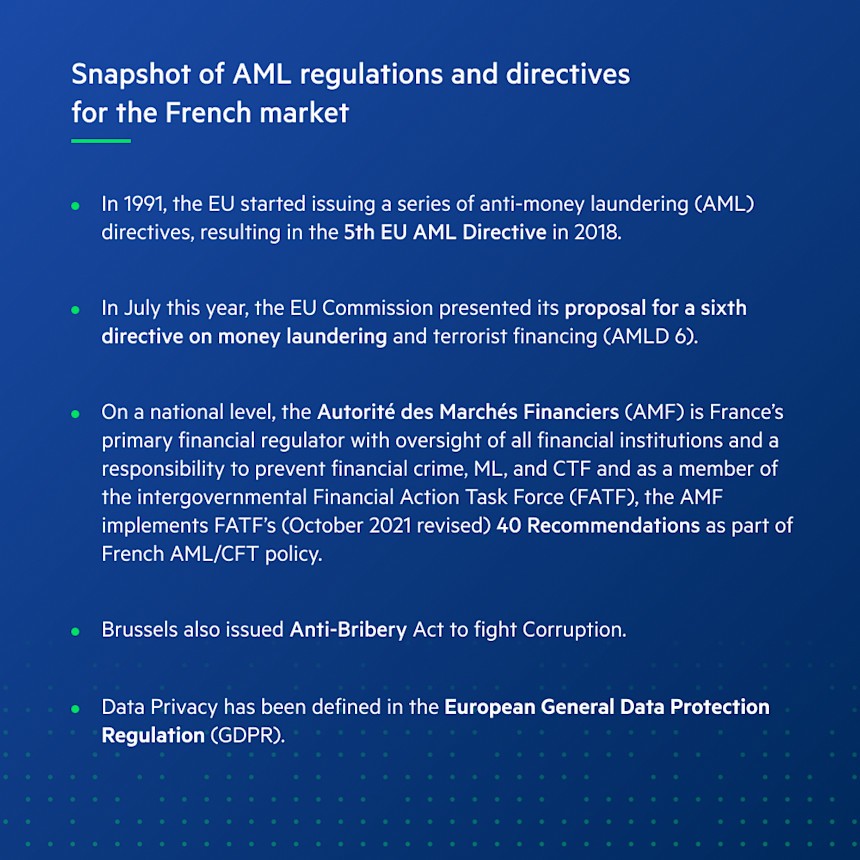

In France, the Monetary and Financial Code and the French Criminal Code have defined regulations to combat money laundering and terrorist financing (CFT) . In France, the parquet national financier, or PNF, has the authority to prosecute money laundering offenses at the national level where funds are obtained through corruption, fraud, or misappropriation of funds.

Financial institutions that operate in France have to comply with French law and with EU Directives. Rules and recommendations often overlap, but there are subtle differences on a national level when it comes to the interpretation and implementation of these directives.

AMF, ACPR and Tracfin

The Financial Authority (AMF) and the Autorité de Contrôle Prudentiel et de Résolution (ACPR) are the primary financial regulators in France. The AMF works closely with domestic and international authorities to further the collective effort against money laundering and has a wide range of powers to conduct investigations and issue penalties. While the AMF is responsible for the supervision of financial markets and investment firms, the ACPR is an independent authority under the Banque de France and supervises the banking and insurance sectors. The AMF and ACPR act in concert with the European Banking Authority (EBA).

The pressure increases for banks, insurance companies and real estate

French insurers are under mounting pressure, now that the ACPR recently disclosed that it will double onsite inspections. Last year, ACPR discovered that almost one third of intermediaries or brokers sell life insurance or investment bonds, but only a minority had designated AML officers on board to flag suspicious transactions to Tracfin, France’s financial intelligence unit. In March, the French ACPR handed ING France a €3m fine for failing to implement sufficient controls to prevent money laundering. Their annual report revealed that French Real Estate companies fail to clamp down on illicit funds. Tracfin concluded that private banks and money exchangers in France had submitted fewer suspicious activity reports while most other regulated businesses increased their reporting volume.

Financial institutions that fail to monitor and report suspicious activities face considerable financial and reputational risk. An in-depth investigation by a collective of European news outlets called the Organised Crime and Corruption Reporting Project (OCCRP) revealed a money-laundering scandal that involved several respected European banks. The OCCRP report was based on leaked documents detailing transactions worth more than $470bn sent in 1.3 million transfers from 233,000 firms. Major Dutch and Scandinavian banks, the Deutsche Bank, the RBI, Scottish RBS and the French Credit Agricole were affected by this money-laundering scandal.

Customer Due Diligence (CDD/KYC/AML)

Financial institutions have to implement a solid Customer Identification Program (CIP) as part of Customer Due Diligence (CDD) to prevent money laundering and terrorist financing. Before a customer is accepted (onboarded), risk professionals verify the ID of the new customer, perform screening and assess potential (low, medium, high) risk.

The rising threat of document fraud increases the pressure on CDD and ongoing monitoring. Manual procedures often lack speed and precision. This is why financial institutions increasingly choose to integrate automated Regtech solutions to improve efficiency and reduce costs.

Document ID fraud

The Covid-19 pandemic saw a surge of fraud in the application process through the use of forged identity documents. Organizations dealing with French applicants are more likely to deal with fake identity documents in higher quantities. Currently, France does not have a central identity card repository for data storage: the lack of a single, shared location for identity checks contributes to fragmented and time-intensive KYC processing. Document fraud is rising and has now surpassed identity fraud cases, making document fraud more prevalent in France than any other European country.

Enhanced Due Diligence/Ongoing Risk Monitoring

Under AFM regulations and the Action Plan against Money Laundering and Terrorist Financing 2021 – 2022, financial institutions that operate in France must include risk monitoring as part of their CDD program.

During Risk monitoring, relevant information is extracted from large amounts of data that is analyzed to calculate and assess risk. Risk has to be scored and unusual patterns have to be detected. Manual Risk Monitoring is cost- and time-inefficient and prone to human error.

When France is your company’s first stop in the European Union.

AML and KYC regulations and compliance requirements in France can get rather complex for firms that want to expand their footprint into the French market. Particularly when France is your first stop in the European Union. This is why companies increasingly choose to partner with a regulatory compliance solutions provider. A Regtech with extensive knowledge of the European legal landscape can offer solutions and guidance.

Fintech innovation

Last summer, ACPR’s Fintech Innovation Hub organized a Tech Sprint about the use of Artificial Intelligence and Machine Learning in the battle against financial crime and non-compliance. This initiative confirms the growing importance of Regulatory Technology to support financial institutions’ compliance with AML, CTF and CDD rules and regulations.

Fourthline is a Regtech solutions provider with two regulatory licenses, which enables us to help our customers engage with regulators and carry out cross-country operations, in compliance with the requirements defined by French regulators. Only recently, Fourthline partnered with the French National Police to strengthen joint efforts in tackling financial crime. Our end-to-end AML/KYC Due Diligence and Fraud Detection solutions support smooth expansion into new territories like France, while preventing the risk of non-compliance. Our powerful backend automation processes do all the legwork for you, dramatically reducing your total cost of compliance and freeing up your time to focus on your core business.