Feb 12, 2024

How Tier 2 banks can leapfrog larger competitors with specialized KYC and compliance solutions

The Fourthline Team

Compared to their Tier 1 counterparts, they are more nimble and are adding meaningful volumes of new clients. And they are frequently more stable and seen as more trustworthy than fintechs by their clients.

However, there are strategic risks to this market position. For example, fintechs are more aggressive in adding new clients and faster in rolling out new features. As fintechs build trust and develop sustainable business models, they will capture market share away from established banks. On the other hand, in a financial crisis Tier 2 banks don’t necessarily have the safe haven status of Tier 1. During such a situation, there is a real risk of losing clients to larger competitors, or even worse, experiencing a bank run at a critical moment, particularly if regulators decide to focus on protecting bigger banks.

And finally, even in business-as-usual situations, Tier 2 banks are facing unsustainable costs of compliance. This includes the constant investment needed to maintain and upgrade systems due to evolving regulations. Frequently, costs that are assumed to be one-off prove to be ongoing as banks that ramp up teams and investments through remediation challenges fail to bring down costs afterwards. For example, with remediation challenges, banks often hire consultancies such as KPMG or Deloitte to perform manual document renewals, or comb through data to fix inconsistencies.

The big opportunity in KYC and remediation

Against this backdrop, there is a big opportunity for Tier 2 banks to bring down the exorbitant existing costs of compliance, become more competitive, and future-proof their business. Today, there are a number of dedicated KYC and remediation solutions built by specialized providers such as Fourthline, which have been leveraged by banks and fintechs alike for years. Working with solutions such as these offers a compelling option to Tier 2 banks for several reasons:

Cost-effectiveness

Tier 2 banks don’t always have the resources of Tier 1 banks. But this bug can be turned into a feature. Partnering with a specialized provider is always more cost-effective than building in-house. Therefore, with this approach, you are achieving two objectives simultaneously; keeping your overheads low while delivering the solutions you need.

Speed

Banks always have multiple competing priorities and, frequently, long roadmaps. Added to this is the aforementioned issue that Tier 2 banks frequently have fewer resources than Tier 1 banks so they need to be more creative in order to compete. Partnering with a proven provider is a way to sidestep lengthy building processes and roll out the solutions you need quickly.

Customer experience

Banks have a broad range of services to provide and complex challenges to solve. In comparison, specialized providers, such as Fourthline, are focused on solving a relatively small number of challenges exceptionally well. As such, they can provide better KYC and remediation experiences for banks’ clients.

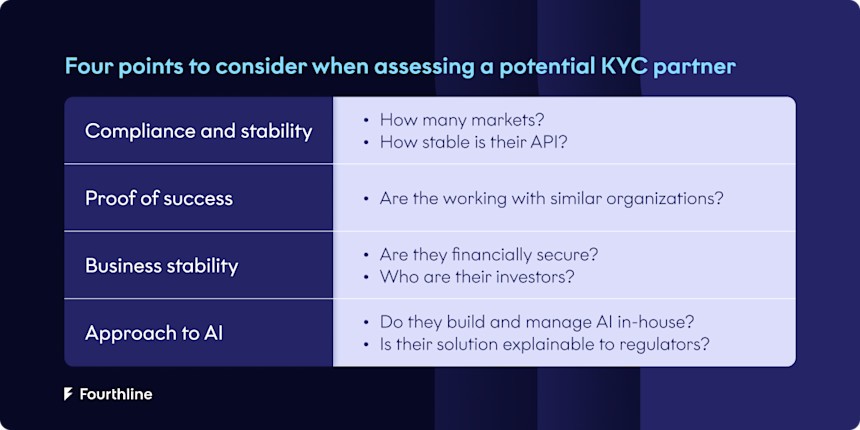

How to assess the suitability of a potential KYC and remediation partner

While these benefits are compelling, there are, of course, some critical points to consider when assessing potential partners.

Compliance and stability: Above all else, it is critical that you can trust your partner. Considerations include the markets in which your partner is regulated and/or licensed and how stable their API is - including redundancy and how many cases they can process successfully at a given time.

Proof of success: If your provider is already successfully delivering similar solutions for organizations like yours, it inspires greater confidence in their offering.

Business stability: A partner running into financial trouble can also have serious negative consequences for your business, so it’s important to make sure they are stable.

Approach to AI: This is now an essential component in KYC/compliance solutions, so you need to ensure your partner has an approach that balances innovation and security.

Why Fourthline may be a suitable partner

Fourthline is already processing millions of KYC and AML cases, in line with regulatory requirements, for a range of clients, including several Tier 2 banks, and is backed by a recent investment from institutional investors. Further, we have been investing in AI for years, with technology built and maintained in-house, and have a structured approach to data integrity and ethical practices.

In terms of customer experience, our KYC solution offers an easy, non-intrusive flow that includes an ID check and selfie and, in some markets, bank account verification, qualified electronic signature, and physical proof of address. In the background, Fourthline performs over 200 checks on every identity verification, checking for authenticity, security features, liveness, and more. 90% of these are performed automatically in real-time. And, with our fully automatic remediation flow, Fourthline completes customer files without any action required from the client.

This means big benefits for clients. According to a commissioned study by Forrester Consulting on behalf of Fourthline, Fourthline can deliver an ROI of almost 400%, along with 75-95% reductions in the cost of compliance. On top of that, our solutions can be delivered at speed. Several Tier 2 banks have partnered with us during moments when they faced regulatory scrutiny and the possibility of significant fines if strict deadlines could not be met.

KYC and remediation are opportunities for Tier 2 banks to future-proof businesses and reduce the cost of compliance now

If there is one more thing for Tier 2 banks to consider, it’s that conversations with specialized compliance partners do not need to wait for a crisis to occur. Starting a collaboration with a partner is easier without the pressure of potential fines or regulatory scrutiny. Further, providers, such as Fourthline, offer modular solutions that can be launched at a small scale and evolve as needed, meaning you can see ROI with very little risk. With such an approach, the result is lower costs for banks, and better experiences and security for your clients.

If you’d like to discuss your challenges around KYC and remediation, contact us.